News

Recently, the US Census released the results of its monthly Value of Construction Put in Place Survey. The survey provides estimates of the total dollar value of construction work done in the U.S. This data includes design and construction spending for public and private projects.

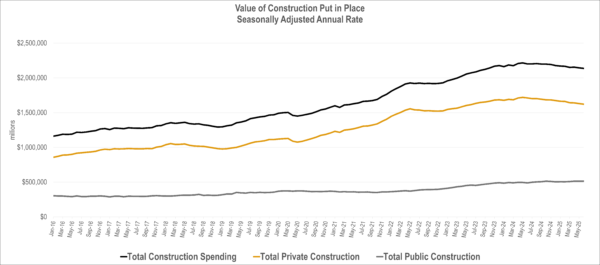

The seasonally adjusted annual rate of $2.14 trillion for June 2025 represents a monthly decline of -0.4%. Due to revisions, this is the 2nd consecutive month of decline for the growth rate; however, over the past 12 months, the month-over-month (MoM) growth has been negative or flat 10 times.

This value also represents a -2.9% decline in year-over-year (YoY) growth. This is now the 5th consecutive month of year-over-year declines. Looking at historical data, the current spending cycle peaked in May 2024 at $2.22 trillion. The current seasonally adjusted spending rate is -3.6% below that peak.

The last time there were 5 or more months of consecutive YoY declines was Nov 2018 through April 2019. Private construction saw a MoM decline of -0.5% while Public construction grew 0.1%.

Source: US Census Value of Construction Put in Place Survey August 1, 2025 release

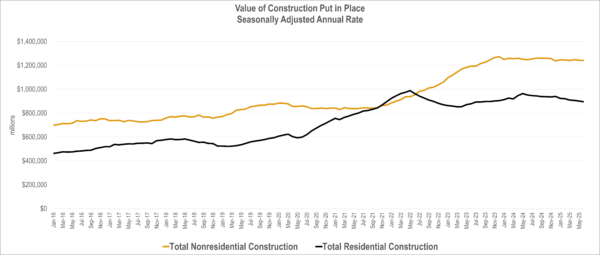

This decrease in growth highlights the uncertainty for the current economic climate. After a contraction in real GDP growth in the 1st quarter of 2025 of -0.5%, the first estimate for the 2nd quarter of 2025 was 3.0%.

Factors such as higher-for-longer interest rates, changes in fiscal policy, trade uncertainty, and other economic conditions are impacting the majority of markets to varying degrees. The residential market declined -0.7% month over month while the nonresidential market declined -0.1%.

Source: US Census Value of Construction Put in Place Survey August 1, 2025 release

With respect to year-to-date growth in individual markets, 2025 continues a shift away from sectors that previously lead growth and new sectors emerging. The Water sector continues to grow in both Supply and Sewage & Waste Disposal, while growth in Amusement & Recreation remains strong and Public safety is a top growth market, replacing Transportation.

With the most recent update, 8 out 17 sectors have year-to-date declines in total spending. Commercial continues to see declines due to interest rate sensitivity and other secular trends affecting demand. The Residential sector is seeing declines after rebounding from Spring 2023 lows, while Manufacturing is now seeing declines after significant growth during 2022-2024.

Date

August 6, 2025

Category

ACEC NEWS / EDUCATION / MARKET FORECAST